Stocks Strategy - AI World

Month June of no opinion, just math. Monthly execution log of US public equities investment strategy

FICH Public Equities is a systematic, long-only investment strategy that trades exclusively within the S&P 500 universe. The algorithm evaluates relative strength every month and automatically rotates capital into the 10 most dominant stocks, maximizing exposure to leading macro trends while completely removing human bias.

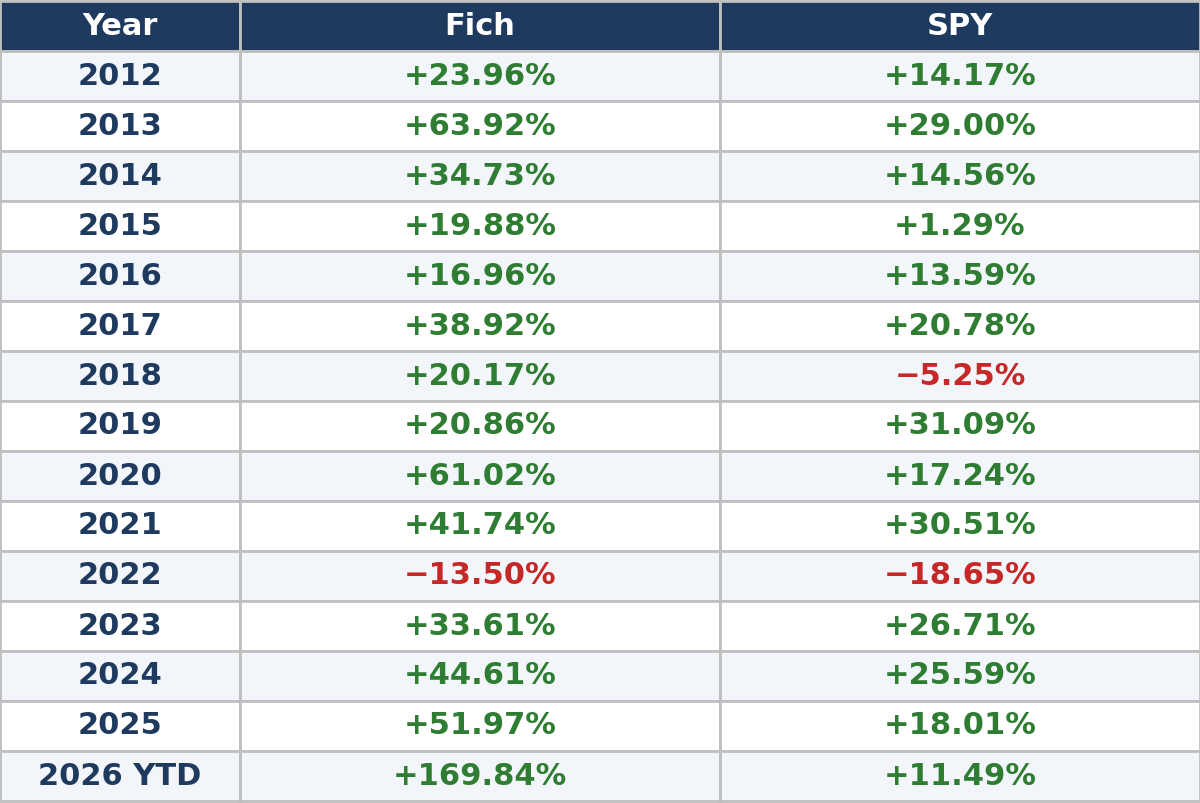

Annual Returns - Fich Strategy vs SPY

1. Macro Overview

U.S. equities extended strong gains into early June 2026: S&P 500 rose about 5.7% over the past month, Nasdaq led with tech-driven momentum near record highs, and the Dow posted more modest advances.

Market leadership remained highly concentrated in technology, especially semiconductors and AI infrastructure, which rose roughly 16–17%, while most other S&P 500 sectors were flat to down.

The 10-year Treasury yield stayed elevated around 4.4%, reflecting steady rate expectations amid geopolitical oil-price volatility; energy stocks were pressured as crude moderated from earlier spikes following ceasefire and supply developments.

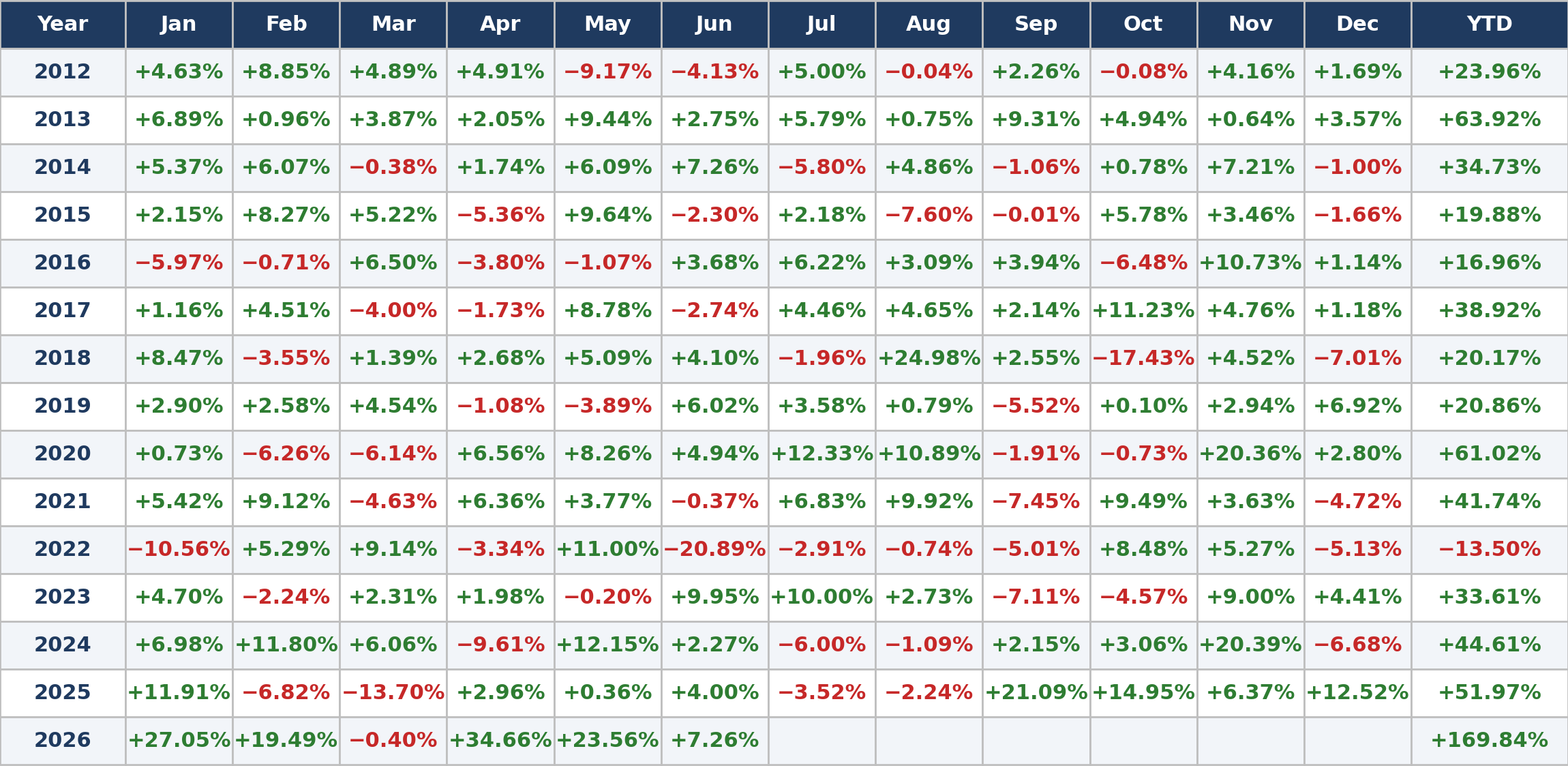

Fich Monthly Returns (2012 – present)

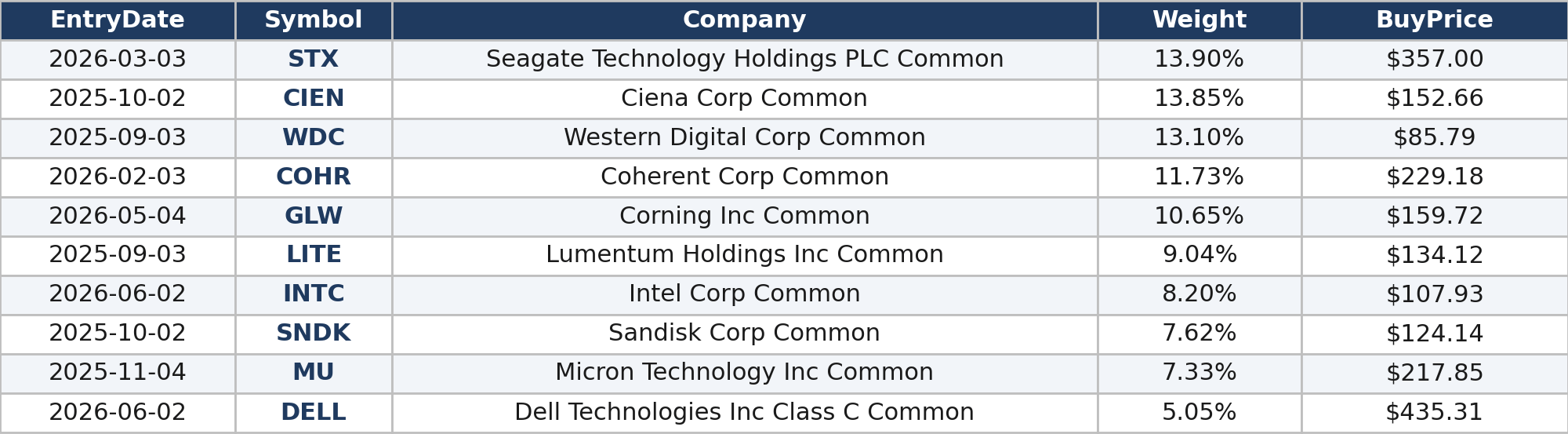

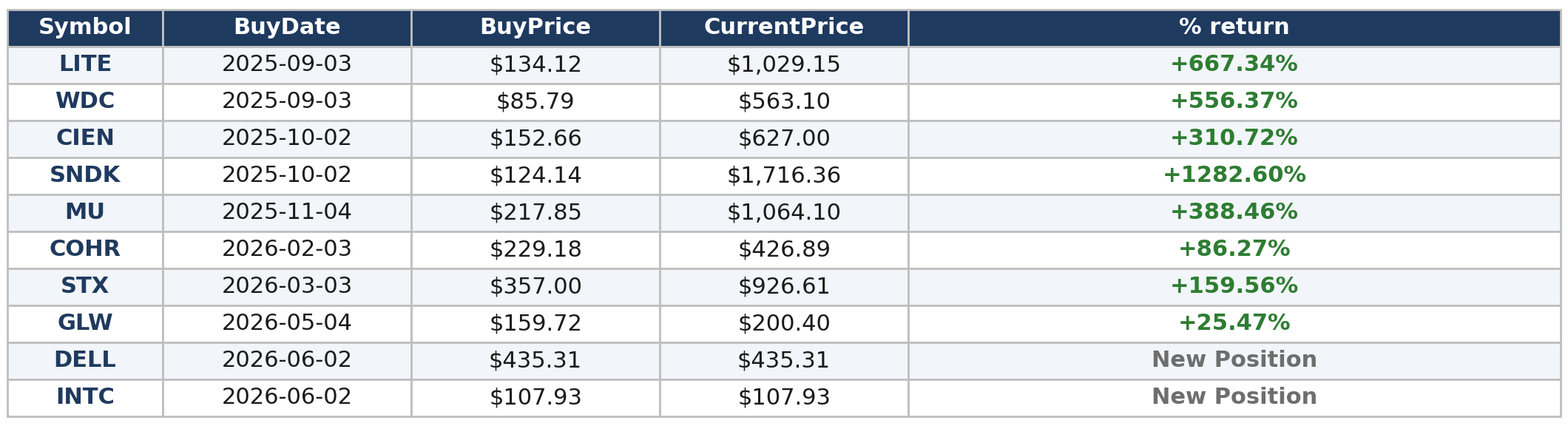

2. The Portfolio: Current Holdings (June 2026)

The dominant theme across our technology pillars is a structural, multi-year hardware upcycle driven by the simultaneous acceleration of AI adoption, exponential data creation, and the urgent modernization of cloud and telecommunications infrastructure. Capital is being pulled toward the foundational layers of the digital economy—advanced semiconductor manufacturing, high-bandwidth memory, optical networking, and enterprise data storage—as hyperscalers and network operators race to build AI training and inference capacity that demands unprecedented compute density, ultra-low latency interconnects, and massively scalable, reliable storage. In this environment, the key signal is not incremental software innovation but the expanding physical requirements of AI and cloud workloads, which elevate the strategic importance of the “picks-and-shovels” suppliers that provide silicon, memory bandwidth, optical transport, and storage architecture. We view these components as indispensable infrastructure for the modern cloud and global data transport, positioning the portfolio for continued demand as the industry invests in the materials, fabrication, and server-grade systems that enable the next wave of software breakthroughs.

Portfolio Breakdown

STX (Seagate Technology Holdings plc) — Weight: 13.90% delivered fiscal Q3 2026 revenue of $3.11 billion with non-GAAP gross margin of 47.0% and non-GAAP diluted EPS of $4.10, exceeding forecasts on robust demand for mass-capacity storage in AI and cloud environments. Operating cash flow was $1.1 billion, supporting $641 million in debt retirement and shareholder returns. The results highlight Seagate’s successful positioning in enterprise and data center HDD solutions amid the ongoing AI infrastructure expansion.

CIEN (Ciena Corporation) — Weight: 13.85% posted strong fiscal Q1 2026 results with revenue of $1.43 billion, up 33.1% year-over-year, supported by accelerated AI-driven demand for optical networking, WaveLogic 5 and 6 Extreme platforms in subsea and data center interconnects. Adjusted EPS of $1.35 beat estimates, with notable wins in cloud and subsea projects contributing to significant share price appreciation. Analysts have responded with substantial price target increases reflecting confidence in continued optical networking expansion tied to AI infrastructure buildout; fiscal Q2 2026 results are scheduled for release on June 4, 2026.

WDC (Western Digital Corporation) — Weight: 13.10% reported robust fiscal Q3 2026 results with revenue of $3.34 billion, up 45% year-over-year, driven by AI-driven demand for high-capacity storage solutions. GAAP gross margin reached 50.2% (non-GAAP 50.5%), with non-GAAP diluted EPS of $2.72, exceeding consensus. The company highlighted multi-year agreements extending into 2028–2029, launched industry-first post-quantum cryptography hard drives for AI data security, appointed an AI-focused executive to its board, and guided for approximately 40% year-over-year revenue growth in fiscal Q4, reflecting sustained momentum in cloud and enterprise storage.

COHR (Coherent Corp.) — Weight: 11.73% reported fiscal Q3 2026 revenue of $1.81 billion, up 21% year-over-year (27% pro forma), with continued strength in lasers and photonics for industrial, communications, and AI-related applications. GAAP gross margin improved to 37.7% and non-GAAP EPS reached $1.41, beating expectations. The company provided Q4 guidance of $1.91–$2.05 billion in revenue and non-GAAP EPS of $1.52–$1.72, reflecting solid execution amid broader optoelectronics tailwinds.

GLW (Corning Incorporated) — Weight: 10.65% announced strong Q1 2026 results with core sales of $4.35 billion (up 18% year-over-year) and core EPS of $0.70 (up 30%), propelled by robust Gen AI product demand and the ramp of new solar offerings. GAAP sales were $4.14 billion. While Q2 guidance incorporates a planned maintenance shutdown, the underlying momentum in optical communications, specialty materials, and AI-related glass applications remains positive, reinforcing Corning’s diversified growth profile.

LITE (Lumentum Holdings Inc.) — Weight: 9.04% delivered exceptional fiscal Q3 2026 results ended March 28, 2026, with net revenue reaching $808.4 million, representing 90.1% year-over-year growth and 21.5% sequential increase, fueled by surging demand for optical components in AI infrastructure and data centers. GAAP gross margin stood at 44.2% with non-GAAP at 47.9%, while non-GAAP operating margin expanded to 32.2% and non-GAAP diluted EPS hit $2.37, beating estimates. The company joined the Nasdaq-100 Index, saw multiple analyst price target upgrades (often exceeding $1,000), and provided strong Q4 guidance of $960 million–$1.01 billion in revenue with non-GAAP EPS of $2.85–$3.05, underscoring its pivotal role in photonics for AI networking.

INTC (Intel Corporation) — Weight: 8.20% reported Q1 2026 revenue of $13.6 billion, up 7% year-over-year, with non-GAAP EPS of $0.29. While facing ongoing competitive pressures in foundry and client segments, the company is advancing its process technology roadmap and benefiting from broader AI ecosystem tailwinds, with shares showing substantial year-to-date appreciation. Guidance for Q2 2026 projects revenue of $13.8–$14.8 billion, as management continues restructuring and strategic initiatives to restore competitiveness in semiconductors and AI acceleration.

SNDK (SanDisk Corporation) — Weight: 7.62% achieved record fiscal Q3 2026 performance with revenue of $5.95 billion and non-GAAP diluted EPS of $23.41, significantly surpassing estimates amid explosive AI memory demand. The data center segment grew 233% sequentially, gross margins expanded dramatically to 78.4%, and the company secured over $42 billion in future revenue commitments. Shares have delivered extraordinary gains exceeding 4,000% over the past year, with analysts raising price targets substantially (up to $3,250) and upgrading ratings, while management initiated a $6 billion share repurchase, affirming strong positioning in high-bandwidth memory and storage for AI.

MU (Micron Technology, Inc.) — Weight: 7.33% reported record fiscal Q2 2026 results (ended February 2026) with revenue of $23.86 billion—nearly tripling year-over-year—driven by unprecedented AI memory demand across DRAM and NAND. GAAP net income reached $13.79 billion ($12.07 per diluted share) and non-GAAP EPS $12.20, with gross margins approaching 75%. The company guided for even stronger sequential performance and continues to benefit from supply constraints and high-value AI infrastructure spending, positioning it as a core beneficiary of the memory supercycle.

DELL (Dell Technologies Inc.) — Weight: 5.05% exhibited explosive AI server growth in its fiscal Q1 2027 results (reported May 2026), with overall revenue surging to $43.84 billion (up ~88% year-over-year) and non-GAAP EPS reaching $4.86. AI-optimized server revenue alone jumped 757% to $16.1 billion, driving the company’s fastest revenue growth pace since its 2018 relisting. Full-year fiscal 2027 guidance was raised materially, underscoring Dell’s leadership in AI infrastructure hardware and services, with shares reacting strongly to the accelerated outlook.

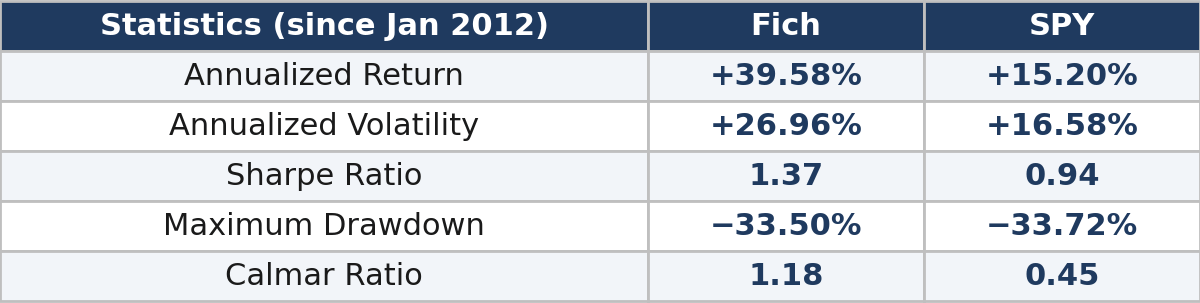

3. Performance and Statistics

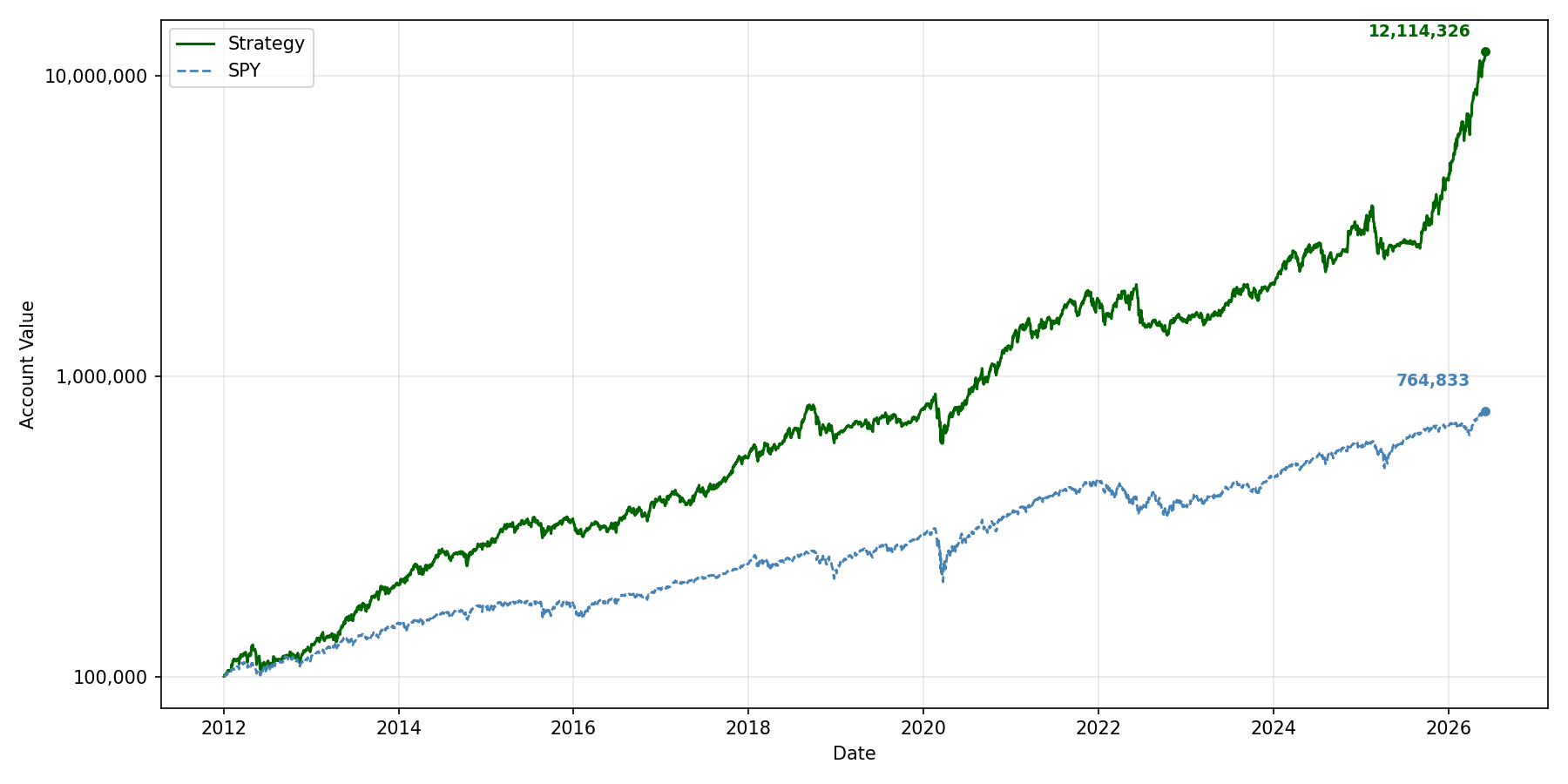

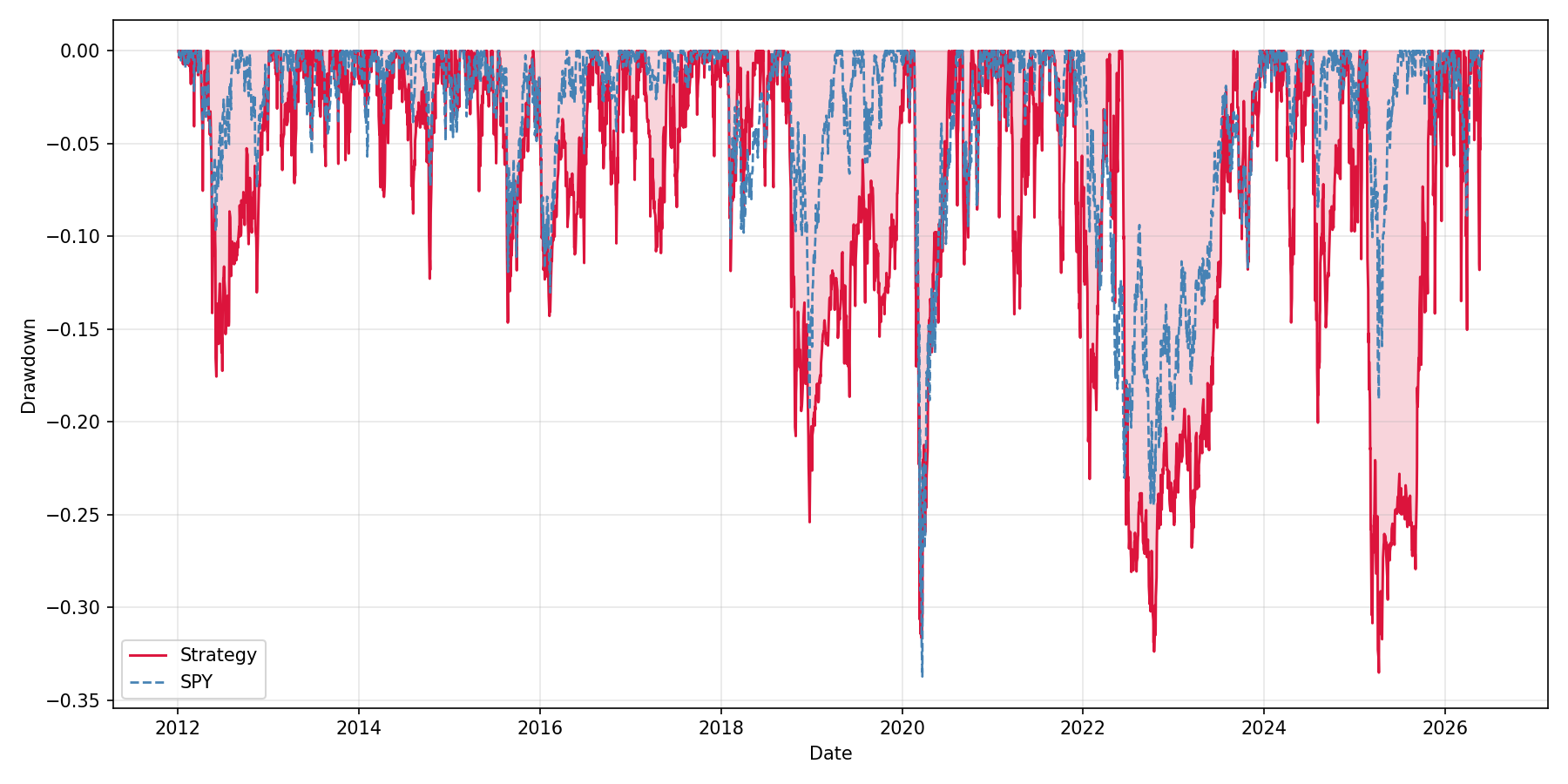

Since January 2012, Fich Public Equities investment strategy has systematically compounded a simulated $100,000 starting portfolio into over $11.29 Million, achieving an annualized return (CAGR) of 39.58% while strictly capping the historical maximum drawdown at −33.50%.

Current Portfolio Performance

Equity Curve - Fich vs SPY

DrawDown Curve - Fich vs SPY

Disclaimer: Past performance is not indicative of future results. All strategy performance metrics and stated returns are net of a 0.10% commission fee per trade. For comprehensive historical data and complete execution logs, visit fich.ai.