Stocks Strategy - New Approach to the S&P 500 Universe

Month July of no opinion, just math. Monthly execution log of US public equities investment strategy

Due to significant inbound institutional interest in our investment models, we have refined our public equities strategy to execute strictly within the S&P 500 universe. This structural adjustment ensures that our portfolio parameters meet the strict liquidity and volume thresholds required for large-scale capital deployment.

FICH Public Equities is a systematic, long-only investment strategy that trades exclusively within the S&P 500 universe. The algorithm evaluates relative strength every month and automatically rotates capital into the most dominant stocks, maximizing exposure to leading macro trends while completely removing human bias.

Annual Returns — Fich Strategy vs SPY

1. Macro Overview

Over the past 30 days (primarily June 2026), major U.S. equity indices showed mixed performance amid a broadening of market leadership: the S&P 500 fell about 1%, the Nasdaq fell around 2.8%, while the Dow Jones rose roughly 2.7% and the Russell 2000 advanced about 3.7–4.2%.

The market rotated away from mega-cap growth and technology concentration (including pressure on the Magnificent 7 and hyperscalers) toward cyclical, value, and small-cap segments, with more stocks declining than advancing over the month.

Sector performance showed strong outperformance in Industrials (+7.3%) and Health Care (+6.6%), with additional gains in Financials and Utilities; Energy (-5%), Communication Services (-7.2%), and parts of Consumer Discretionary weakened.

U.S. Treasury yields rose modestly at the front end with the 10-year around 4.5–4.6%; global government bonds posted small gains, while commodities (including oil) fell sharply.

Algorithmic positioning favored Industrials, Health Care, Financials, and value-oriented small, while reducing exposure to concentrated growth areas, particularly large-cap Technology and Communication Services, amid divergence within the AI trade (semiconductors relatively resilient in spots but hyperscalers under pressure).

Overall, the environment reflects a transition from narrow leadership to more distributed capital allocation, with exposure tilted toward sustained momentum and away from areas with decaying relative strength.

Fich Monthly Returns (2012 – present)

2. Last month overview: Fich Equities vs the market

In June 2026, Fich Equities strategy returned +15.27% in June, against −1.03% for the S&P 500.

Stepping back to the year-to-date picture:

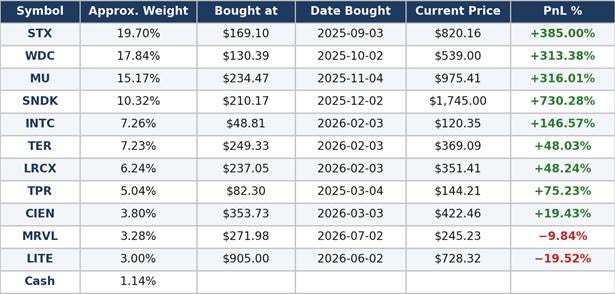

3. The portfolio at this rebalancing: bought, sold, and held

On 10 July, the system held 11 from the previous months, leaving the portfolio at roughly 1.14% cash.

The algorithm systematically closes underperforming stocks while holding positions with strong momentum.

Current portfolio:

Portfolio update

STX (Seagate Technology) - Weight 19.7%. Seagate has delivered exceptional performance amid surging AI-driven demand for data storage, with its stock rising over 500% in the past year and recently trading near $860–$915. Fiscal Q3 2026 results showed revenue of $3.11 billion (up 44% YoY), non-GAAP EPS of $4.10 (beating estimates of $3.50), and gross margins expanding to 47%. The company highlighted strong free cash flow of $953 million and reiterated robust guidance, while announcing exchanges and redemption of exchangeable notes in May–June 2026. Multiple analyst upgrades, including Buy initiations from Melius Research and significant price target increases (to $1,300 from Cantor Fitzgerald and $1,150 from BofA), reflect optimism around HAMR technology and tighter HDD supply. Leadership changes included the retirement of long-serving independent director Michael R. Cannon.

WDC (Western Digital) - Weight 17.84%. Western Digital has capitalized on the AI storage boom, with its stock more than tripling in 2026 and recently trading in the $550–$600 range following strong momentum. Fiscal Q2 2026 revenue reached $3.02 billion (up 25% YoY), with non-GAAP gross margin of 46.1% and upbeat Q3 guidance at the midpoint of $3.2 billion revenue. The company reported 2026 HDD capacity fully sold out and showcased AI-optimized solutions at Computex 2026, including high-capacity Ultrastar HDDs and tiered storage architectures. It was added to the 2026 S&P Dow Jones Best in Class Index for sustainable AI infrastructure. Multiple bullish analyst actions, including Buy initiations from Melius Research and price target hikes (to $900 from Cantor and $730+ from Wells Fargo/BofA), underscore expectations for continued growth in data center and AI applications.

MU (Micron Technology) - Weight 15.17%. Micron reported record fiscal Q3 2026 results with revenue of $41.46 billion, more than quadrupling from the prior-year period, fueled by soaring AI memory demand and higher pricing. The company executed transformational strategic customer agreements, accelerated U.S. investments (including pouring first concrete at its New York fab), and announced up to $3 billion in strategic investments plus agreements with Ford and General Motors for long-term supply. A $250 billion investment plan was highlighted to address AI chip demand. Shares have shown extreme volatility but remain up dramatically on the year, with analysts viewing Micron as a core beneficiary of the memory supercycle despite periodic pullbacks tied to sector rotation.

SNDK (SanDisk) - Weight 10.32%. SanDisk has experienced substantial gains driven by AI memory and NAND demand, with shares recently trading above $1,800 after notable volatility. Fiscal Q1 2026 revenue was $2.31 billion (up 21% sequentially), supported by strong datacenter growth and BiCS8 technology ramping to majority of bit production by year-end. The company is qualifying with multiple hyperscalers, with engagements across five major customers. Analysts remain largely bullish ahead of its August 2026 earnings, citing expected revenue growth, NAND pricing gains, and a “very strong quarter,” though shares have faced pressure from broader memory sector selloffs and competition. Goldman Sachs and others have raised targets significantly, positioning SanDisk as a key AI play.

INTC (Intel) - Weight 7.26%. Intel is advancing its multi-year turnaround with a $200 billion plan gaining traction, focusing on foundry leadership and AI innovations. Recent highlights include the debut of Intel 18A in data centers with Xeon 6+ processors, new Arc G3 handheld gaming chips, and AI solutions showcased at Computex 2026. Leadership appointments at Intel Foundry aim to accelerate development, while process milestones were detailed at the VLSI Symposium. Q1 2026 revenue rose modestly to $13.6 billion, with Q2 guidance in the $13.8–$14.8 billion range. The stock has shown resilience amid market rotations but faces pressure from elevated AI spending expectations and competition; analysts are mixed, with some highlighting the foundry story as “too good to ignore.” Earnings are scheduled for July 23, 2026.

TER (Teradyne) - Weight 7.23%. Teradyne reported record Q1 2026 revenue of $1.282 billion (up 87% YoY), driven by $1.111 billion in Semiconductor Test, with GAAP EPS of $2.53 and non-GAAP EPS of $2.56 both exceeding guidance. The company introduced an integrated test solution for AI and data center devices in collaboration with Tokyo Electron in June 2026 and was named a 2026 VETS Indexes Recognized Employer. Strong demand for AI compute is expected to accelerate in H2 2025 into 2026. Analysts have raised price targets aggressively (to $550 from Susquehanna and Cantor Fitzgerald), reflecting bullish sentiment on semiconductor test growth amid the AI cycle. Q2 guidance was raised, supporting an 81%+ YTD stock gain.

LRCX (Lam Research) - Weight 6.24%. Lam Research continues to benefit from semiconductor equipment demand tied to AI, with its June-quarter earnings call scheduled for July 29, 2026. The company established a Panel-Level Packaging Center of Excellence in Salzburg, Austria, in May 2026 and declared a quarterly dividend of $0.26 per share. Recent analyst actions include price target increases (to $404 from Morgan Stanley), though the stock has faced volatility from China export rules and sector pullbacks. Management is focused on innovation in wafer fabrication equipment to support advanced nodes and AI infrastructure, positioning Lam for sustained growth as memory and logic spending expands.

TPR (Tapestry) - Weight 5.04%. Tapestry, parent of Coach and kate spade, reported strong fiscal Q3 2026 results with revenue of $1.9 billion (up 21%, or 25% pro forma), double-digit growth in operating profit and EPS, and raised full-year guidance. Coach drove 31% revenue growth in the quarter. The company was awarded a U.S. patent for its proprietary AI platform Mira in May 2026, which integrates data for rapid decision-making in assortment, inventory, and trend response. Additional highlights include the appointment of Matt Madrigal to the board in April 2026 and the launch of AndCoach to engage Gen Z consumers. Tapestry returned $1.3 billion to shareholders and improved inventory turnover, demonstrating disciplined execution in a competitive luxury market.

CIEN (Ciena) - Weight 3.8%. Ciena has delivered exceptional returns, with its stock surging approximately 460% over the past year on the back of a $7.7 billion order backlog and robust hyperscale demand for AI-ready optical networking. Fiscal Q2 2026 results modestly beat estimates but guidance slightly disappointed some investors, leading to post-earnings volatility; full-year revenue guidance was raised to $6.3 billion (±$100 million). The company is scaling its data center connectivity portfolio, introduced Blue Planet Configuration and Change Management, and highlighted AI-driven 5G network slicing for long-term growth. Leadership updates include new appointments for Chief Supply Chain Officer and Chief Product/Technology Officer. While valuation concerns exist, the AI networking tailwinds remain a primary driver.

MRVL (Marvell Technology) - Weight 3.28%. Marvell has raised its revenue outlook on strong AI infrastructure demand, with shares surging over 16% on the update and trading at elevated levels. At Computex 2026, Chairman and CEO Matt Murphy keynoted on AI scaling and connectivity. The company announced the industry’s first 102.4 Tbps switch for AI/cloud data centers in June 2026, declared its quarterly dividend, and is undergoing a CFO transition. Recent shipments of 5 million tower PICs for AI data center optics underscore momentum in photonics and custom ASICs. Analysts are optimistic about new growth engines in data center, though comparisons to peers like Broadcom highlight valuation considerations.

LITE (Lumentum Holdings) - Weight 3.00%. Lumentum has been a standout AI optics beneficiary, with its stock skyrocketing approximately 700–730% over the past year and recently trading near $770–$800 (market cap ~$60 billion). The company is expanding co-packaged optics as a potential next growth driver and continues to lead in AI-related optical components alongside peers. It joined the Nasdaq-100 Index, reduced convertible debt via share exchange, and saw its Chair and CEO participate in the Rome Conference on AI, Ethics, and Governance in June 2026. Analysts have raised targets (to $1,200 from Northland) and view pullbacks as buying opportunities, citing its critical role in solving AI data center bottlenecks despite high valuations (trailing PE ~136, EPS $5.66). Fiscal Q3 2026 results are expected in mid-August.

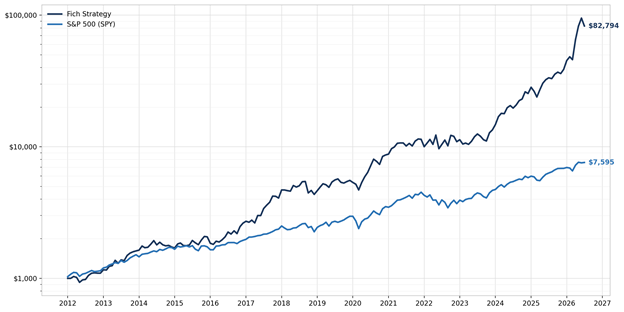

4. Multi-year track record

As of yesterday, that hypothetical $1,000 was worth $82,793.53 in the strategy, versus $7,594.98 in S&P 500.

Fich Equities Strategy vs. SPY - growth of $1,000 since inception (log scale).

Disclaimer: Past performance is not indicative of future results. All strategy performance metrics and stated returns are net of a 0.10% commission fee per trade. This letter is for informational purposes only and does not constitute investment advice. For comprehensive historical data and complete execution logs, visit fich.ai.